It is always like a dream come true when you purchase your favorite car. You just can’t get enough of the fresh-car fragrance, for some reason. You can’t wait to test-drive your favorite car. Even if you spend a lot of money on it, it’s quickly forgotten. Unless you purchased the car completely, you have to pay consistent monthly payments until the remaining amount is paid in full.

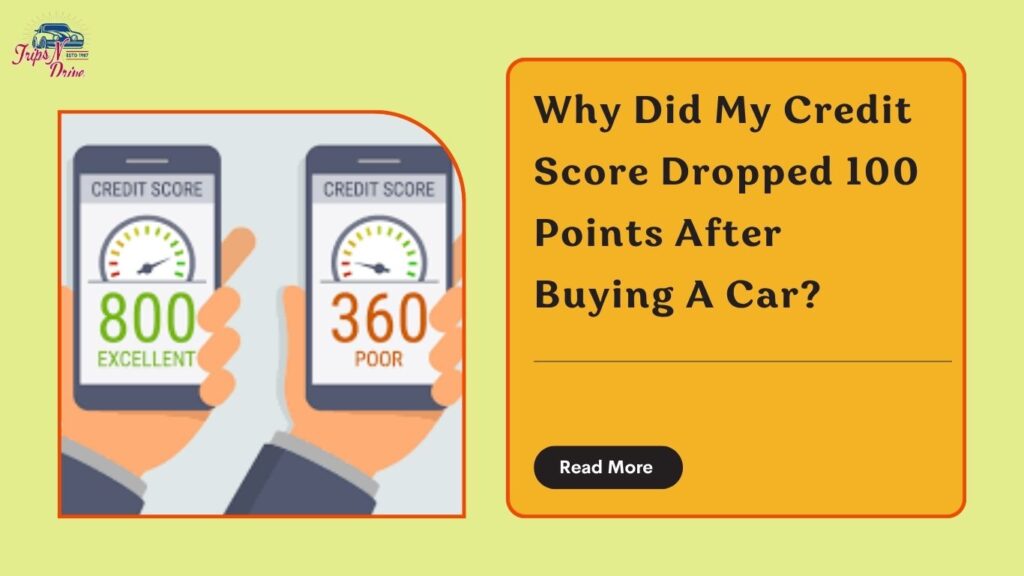

Then you realize that after purchasing a car, your credit score fell by 100 points. Why would something happen that way? But you should be aware that a 100-point decline might have a negative impact on your capacity to borrow money, regardless of the credit score you’re now considering. Therefore, this article will discuss the precautions to prevent credit score dropped 100 points after buying a car.

Reasons For The Drop In Credit Rating

A sharp decline of credit score dropped 100 points after buying a car is not a good sign. Below we have mentioned a few of the reasons why your credit rating saw a sharp decline:

Hard Inquiry On Your Credit Reports

Lenders check your credit history to determine your capacity to pay before approving you for a vehicle loan. When they do so, an intensive inquiry takes place, which credit reference agencies classify as “new credit.”

Your credit score might be substantially reduced by only one hard enquiry. If your credit history is strong overall, it will have less of an effect on your credit score. According to FICO, hard inquiries have an impact on your credit score for the first 12 months, but after two years they disappear from your credit record.

It’s doubtful that a single hard inquiry would have had a substantial effect on your credit score. However, it’s possible that you generated several harsh inquiries, which affected your credit record. Is it possible that you applied with many lenders in search of the best interest rates?

If several lenders do hard inquiries within a period of 14 to 45 days, it could just register as one hard inquiry and barely affect your credit score. Hard queries, on the other hand, will probably have a negative effect on your credit score if you stretch out them.

Decreased Average Loan Account Age

The average age of your loan accounts is one of the factors that determines your credit score. A better credit score is associated with a longer average age, whereas a lower average age results in a lower credit score. The average age of your loan accounts will probably decrease if you get a car loan.

If you have few loan accounts, opening a new account might have a significant influence on your credit score. This is due to the fact that the new loan significantly lowers the average age of your loan accounts, which lowers your credit limit.

Increase In The Amounts Owed

Your credit profile adds another account with a significant amount of debt when you get a new car loan. Your credit usage ratio is calculated by the credit reference bureau by comparing the amounts outstanding to your credit limits.

The total amount you owe on all of your accounts, the number of accounts with outstanding loan amounts, and the difference between your current installment loan balance and the original loan balance on installment loans (such as auto loans) are additional crucial indicators.

Your credit score first plummets dramatically as the amount you owe rises. It may be the cause of your credit score dropped 100 points after buying a car. However, as long as you continue to pay your bills on time each month, your credit score will rise, which will help you make up for the decline in credit. This implies that you commit to paying all other debts for which you have taken out credit in a timely manner as well.

How Does Purchasing A Car Affect Your Credit?

Your credit score may go up or down over the long run depending on whether you buy a car. That depends on how consistently you make monthly loan repayments. Due to rigorous queries, increased loan amounts, and a rise in the number of loan accounts, having a car loan will temporarily lower your credit score.

If you make your payments on time, your credit score will rise. Because of this, credit reference agencies prioritize payment history when determining your credit score. Consequently, timely and full payments should steadily raise your credit score.

Even if buying a car raises your credit score, there are some negative consequences, such as the following:

Missing Monthly Payments

Your auto loan becomes late if a payment is missed on the due date. The lender could provide you with a brief grace period to assist you start making loan repayments again. The lender will be forced to disclose your delinquent to the credit bureaus, which will lower your credit score, if another full billing cycle goes by without you making a payment.

Defaulting On The Loan

Before putting your loan in default, auto lenders may wait 30 or 90 days. Following a default on your loan, the lender transfers control of your account to debt collectors, who will contact you in order to collect payment.

If you repeatedly default, the lender may take the car back. Late payments, defaults, dealing with debt collectors, and car repossession all lower your credit score and are included on your credit history for a full seven years.

Unaffordable Loan

You probably struggle with other bills if you can’t make your payments on time. That can result in late payments, which lower your credit score. This necessitates a thorough evaluation of your financial situation before making a car purchase. If you’re confident that you can afford the various expenditures associated with owning a car as well as the monthly payments then it will help you.

Tips To Help Raise Your Credit Score after Buying Your Car?

Now you know why your credit score dropped 100 points after paying off car the loan but it’s not difficult to establish a decent credit score, but it’s essential to the condition of your finances.

A good score entitles you to get the loans for your personal needs and reduced personal loan interest rates :-

Make Your Payments On Time

The most crucial thing you can do to improve your score is to pay your payments on time. Both of the major credit card scoring theories, FICO and Vantage Score, consider a person’s payment history to be the most important component in establishing their credit score.

For lenders, an individual’s capacity to make credit card payments on time shows that they are competent to borrow and repay a loan. Your credit score is influenced by a variety of factors, not only your credit card bills. All of your bills must be paid on time.

Set Up Autopay

With so many different due dates and limited time, it might be difficult to remember to pay your instalments of car each month. Fortunately, there is a simple solution: autopay. You can set it up so that you just pay whatever is due if you don’t know if you’ll be able to pay the balance in full.

The same holds true for your utilities: You may set up autopay with the majority of significant providers, which will automatically deduct money on a monthly basis from your savings or checking account (or charge your credit card). Some student loan providers can reduce your interest rate if you set up automatic payments.

Don’t Open Too Many Accounts At Once

FICO include both the number of new account openings as well as the number of credit inquiries, such as requests for credit limit hikes or new financial product applications. Only apply for what you truly need to prevent harming your credit score, as making these sorts of requests typically lowers your score.

Additionally, if you’ve recently created too many accounts, certain issuers may immediately reject you even if you have an excellent credit score.

Check And Dispute Errors

You need to be vigilant and look for any inaccuracies in your credit report that might harm your score since it happens more frequently than you might imagine. Perhaps an overdue payment was made but not updated; perhaps you have outdated data that has to be removed; or perhaps the information is inaccurate—an incorrect name, address, etc.—and is not even yours. These mistakes can occur; therefore, you should be aware that they might happen to your credit.

Pick Up An Affordable Car Loan

One of the finest and most popular ways to raise your credit score is through car financing. The loans not only enable you to drive a reliable car, but they also allow you to show that you are able to make consistent payments over the long term. A borrower’s history of on-time car loan payments is a positive sign for mortgage lenders that they can trust them to handle a larger amount of loan.

Final Thoughts

You now understand why I paid off my car and my credit score dropped. Your credit score could be affected by the lender’s hard investigation of your credit check. Other interesting developments are a decrease in the age of your loan accounts and an increase in the loan amounts. However, Your credit score is just temporarily worse.

Still if you have any doubt or feedback please do comment and share with your friends.

Frequently Asked Questions

How much does a car loan drop my credit score?

Your credit score can quickly decline as a result of hard queries; often by five points or less. Hard inquiries are seen as a threat by creditors since they show you need money.

Does buying a car hurt your credit?

Every time you apply for new credit, such as a car loan, lenders run a hard inquiry on your credit record. Your credit score might be harmed by making too many difficult queries quickly.

Is it normal for a credit score to drop 100 points?

This variation is quite natural and depends on many different factors, such as how much credit you use, how old your accounts are, how many times you have applied for credit, and much more. This indicates very serious negative behaviour on your credit report.

Is 700 a good credit score?

A credit score of 700 or above is typically regarded as good for a score with a range between 300 and 850. On the same scale, a score of 800 or more is regarded as exceptional. The majority of customers have credit scores that are in the 600–750 range.